Japan’s HALO Stocks: Quality Hiding in Plain Sight

Leon Rapp

Portfolio Manager, Platinum Japan Fund

The investment world is trying to assess the effect AI will have on software and SaaS businesses. Given the sharp global derating of these stocks, the conclusion appears to be “sell now, ask questions later.”

This sets off a search for businesses that can thrive in an AI world. Thus the recent emergence of ‘HALO’ or ‘Hard Asset, Low Obsolescence’ stocks – often industrial or material manufacturers that have tangible assets with long lifespans and accumulated process know-how. These are difficult to replicate and provide a margin of safety for investors. “Move fast and break things” may work in the virtual world, but not the physical world.

Japan is replete with such firms and they underpin its industrial competitiveness. We hold several of them – world class industrial powerhouses with wide business moats. We haven’t invested in them as an alternative to software but because Japan’s long-term prosperity can be built on the shoulders of these giants.

AI gets physical

We have a distinctly optimistic long-term investment thesis for Japan. It is poised to implement a technological revolution – one that integrates AI into the physical world and creates new markets and growth opportunities.

In our view, for AI to truly transform an economy it must drive productivity gains in the physical realm. The market currently sees the beneficiaries of the AI revolution concentrated in semiconductor firms and related equipment supply chains. It has yet to fully incorporate the efficiency and productivity gains AI could deliver for the industrial and manufacturing economy. This is an area ripe for disruption and opportunity.

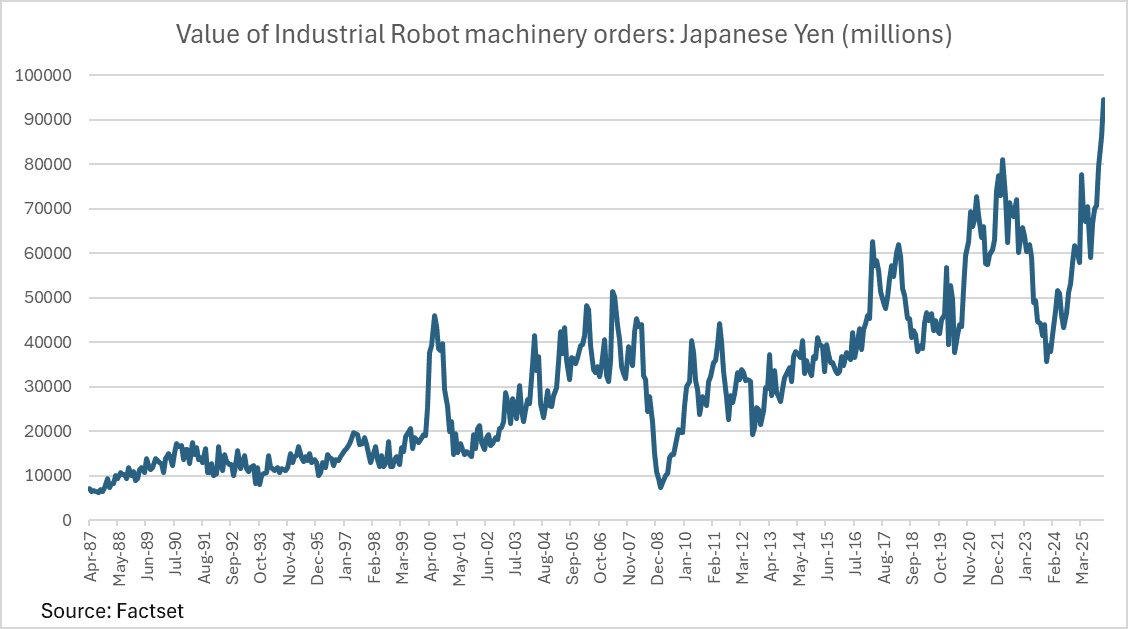

Here Japan’s global leadership in robotics and factory automation technologies – and the productivity increases and cost reductions that come with it – have striking implications.

AI-capable robotics could be used, not just in traditional markets like the auto industry but in light manufacturing, logistics, services and beyond. That increases the addressable market for key Japanese firms by multiples.

Wholesale adoption of these technologies could also invert the economic logic that pushed manufacturing towards jurisdictions with cheaper labour.

Successful development of AI-enabled robotics technologies is a strategic priority for the new Takaichi government. In its AI robotics strategy roadmap released last month, the government targets a 30% global share of a market worth ¥60tr by 2040. Central to this goal is strengthening Japan’s domestic robot supply chain. It also seeks to support demand for robots in manufacturing, aged care, shipbuilding, agriculture and defence.

Make things at home

While Japan is bolstering its technological lead in robots and automation, in the US there’s a clear move away from free trade and towards a more overt industrial policy. For many, the Liberation Day tariffs announced in April 2025 appeared ill-considered, likely to raise import prices and slow investment. We see it as the first step in a longer-term plan to reshore production and reduce supply chain vulnerability.

Subsequent events have strengthened our view. President Trump’s One Big Beautiful Bill Act (July 2025), dramatically increased incentives for capital expenditure in manufacturing. In July, Japan agreed to invest $550 billion in the US in exchange for lowered tariffs. We are already seeing capital being deployed on projects.

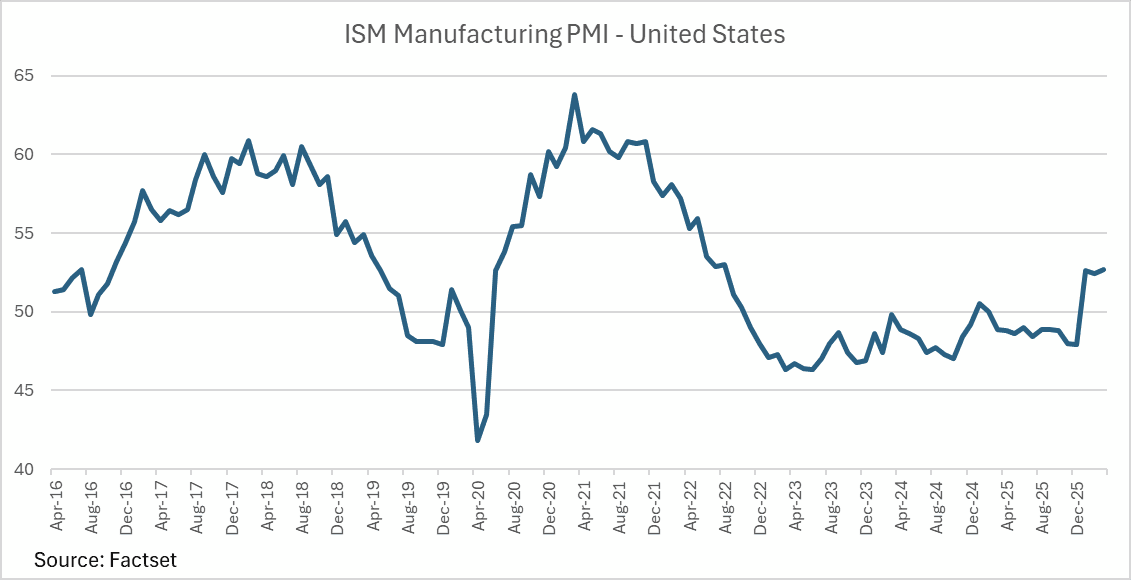

Many were still sceptical of any positive impact from these policies. It was not until the release of the January 2026 US manufacturing PMI that this scepticism was dispelled. It showed a clear shift from contraction to expansion (i.e. over 50).1 We could now be in the first innings of a decade-long shift. The flow-on benefits will be positive for Japanese industrials with the expertise and capital needed to underwrite a US boom.

Reordering the economic order

Over the past 30 years, the relocation of manufacturing to lower-cost countries hurt Japanese and US manufacturers and employment and wages in the sector. Reversing this hollowing out via a reshoring and reindustrialisation strategy could make them beneficiaries of a reordered global economy.

We believe this new policy direction – and the benefits for Japanese industrials – is largely overlooked by global investors. Many of these firms are true HALO companies with deep expertise in production techniques, materials sciences and precision manufacturing. The Platinum Japan Fund is positioned to benefit from this shift. We’re increasing our exposure to key beneficiaries such as FANUC (robotics), Nabtesco (robotic components) and Keyence (factory automation).

Japan reassessed

We now sense a reassessment of Japan’s prospects. We can think of few countries better positioned to benefit from ‘physical AI.’ Japan is dealing with chronic labour shortages which may worsen as the population falls. This may increase the urgency around adopting autonomous AI robotics and result in sharply rising productivity across the economy, providing a net economic benefit.

The transformative leap with AI could also erase the lingering inefficiencies caused by Japan’s previously slow adoption of enterprise IT. Japan’s corporate sector is heavily reliant on customised but inefficient IT systems that are outsourced. Maintaining and integrating legacy systems is a key source of earnings for Japan’s IT services sector. Long viewed as a point of weakness for Japanese corporates, integrating AI into more effective and affordable software solutions would be a welcome development.

Explore the companies shaping Japan’s next era of growth

See how the Platinum Japan Fund invests in businesses at the centre of Japan’s innovation, industrial transformation and long-term economic resurgence.

Share this

1. The Manufacturing Purchasing Managers’ Index (PMI) uses surveys on new orders, production, employment, supplier deliveries, and inventories to gauge the health of the manufacturing sector.

Disclaimer:

The above information is commentary only (i.e. our general thoughts). It is not intended to be, nor should it be construed as, investment advice. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Before making any investment decision you need to consider (with your financial adviser) your particular investment needs, objectives and circumstances.

Related Journals

View all related reads

Platinum Japan Fund | Investor Update

Leon Rapp, Portfolio Manager of the Platinum Japan Fund, discusses the powerful structural shifts reshaping the Japanese economy, key investment themes driving growth, and how the Fund is positioned to capture long-term value in one of the world’s most compelling markets.

Released 18 June 2026.

Japan 2026: A new PM heralds a new golden age?

Former Australian Prime Minister, Paul Keating, once said "When you change the government, you change the country." We're about to see whether that holds true in Japan.¹

Japan’s miracle comeback: What investors need to know

After decades of stagnation, Japan may finally be entering a new era of growth, with corporate reform, rising productivity and industrial renewal creating compelling opportunities for long-term investors.