Douglas Isles provides his latest thoughts on cohesion and its role in building better-performing teams.

In 23 years in financial services, I have worked in five organisations, and interfaced with hundreds more. For about half of my career I have been directly involved in analysing companies as prospective investments. Throughout this journey, it has been clear to me that some teams work together much better than others do. Until stumbling upon cohesion, I had struggled to understand why.

I first came across cohesion in 2015 when I discovered an article by former Wallaby rugby union player, Ben Darwin of data-driven consultancy firm, Gain Line Analytics, stating that England would not win the Rugby World Cup they were hosting that year. As a Scottish Rugby fan, this piqued my interest. Growing up in the UK, I had seen countless repeats of England winning the 1966 Soccer World Cup – England winning is every Scot’s nightmare. As it turned out, Ben was right. In fact, England became the first host nation not to qualify from the pool stages for the knockout rounds.

However, it was the detail behind why Ben didn’t think they could win the World Cup that really caught my attention. His assertion reflected his measurement of how the team was built.

Reflecting on my own industry, simply adding up how many years’ people have been with the firm, or worked in the industry seemed to be the most common ways of demonstrating a team’s strength – a brute measurement of experience.

What I started to learn from Ben was fascinating and it set me on the path of pursuing a deeper understanding of this nascent area of work and its applications to our business, in my quest to quantify Platinum’s strengths.

Ben’s initial observation that had kicked his work off came from tracking how rugby players who transferred clubs performed. This led him to a study by Harvard Professor Boris Groysberg, who wrote the book Chasing Stars: The Myth of Talent and the Portability of Performance.

The “war for talent” intrigued Groysberg. Observing companies’ desperate desire to hire “the best and brightest” into their firms, he chose to investigate the “portability of talent”. If he could determine that talent was robust to a changing environment, then companies were behaving rationally. If not - if the team was bigger than the individual was - then it would suggest a different approach to recruitment and development was appropriate.

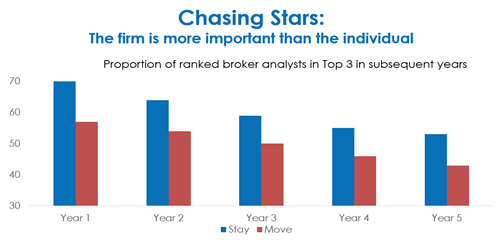

Groysberg’s dataset comprised over 20,000 Wall Street analysts from 1988 to 1996. Since 1972, stockbroking analysts are rated annually in the Institutional Investor rankings. Each year, all ‘star’ analysts are nominated and acclaimed. Being a top-ranking analyst could perhaps add an extra zero to compensation packages that were already obscene in most people’s eyes. Almost everyone in the industry thinks it’s all about an individual’s talents.

Groysberg found that the star analysts saw an immediate degradation in their performance when they switched firms (as the chart below shows). This is despite a culture of paying key individuals millions of dollars in bonuses. Analysts who moved companies found it harder to retain their rankings, than those who stayed where they were.

Source: Boris Groysberg, Chasing Stars: The Myth of Talent and the Portability of Performance

This analysis showed that the star analysts’ client relationships, corporate connections and personal attributes were not enough to overcome internal network, corporate systems, and corporate brands. The firm was more important than the individual was.

In practice, this means hiring people from good firms can be risky, while rescuing good people from inferior firms can be a great opportunity. Ironically, most people have an intuitive sense of this when they craft their CVs, emphasising the most highly regarded firms they have worked for, knowing it inflates perception, and therefore their market value.

So, Gain Line set about measuring cohesion in teams, and they developed two key markers, which have predictive power for team results.

The first marker, Accumulated Continuity measures the combined impact of working together – it grows fastest in smaller units, as relationships are more intense and develop more quickly.

Cohesive teams appear better - they make less mistakes but in addition to building trust, continuity provides more time to focus on improving; stability enables skills development.

The second marker, the Teamwork Index looks at the purity of shared experience within a group.

This idea of purity is important. Relevant external experience is highly sought after, particularly when there are issues that need fixing. Adapting from an old way of doing things is, however, not easy. Quite literally, we have to teach an old dog new tricks - and we all know how hard that is.

Data shows that adding direct external experience can have a negative impact on the team. Sporting teams play in different styles, with different tactics. The new people can find it hard to adapt to the new system and if given enough influence, they will try to make changes to the program to make themselves look better and disrupt everyone else.

These markers are measured, tracked over time and compared within competitions. Gain Line then defines Capacity as “skill times cohesion”, and states that success will be a function of a team’s capacity. Decades of data across sports show that no coach can take a team above its capacity. However, they can certainly (and often do) perform below it.

Gain Line proved to me we can measure the glue with the team and the cohesion markers tell us that we benefit from:

- Time spent together

- Previous experience – with a preference for hiring young, and developing people internally

- Team structure – as small teams develop quickly, a ‘team of teams’ approach can be helpful.

I could see that investment management had a number of similarities with Groysberg’s work. We have a team of analysts organised to look at companies around the world. We have a measurable and systematic, public competition taking place via our performance. There is also a ‘star manager’ dynamic at play, which is exploited to sell successful funds.

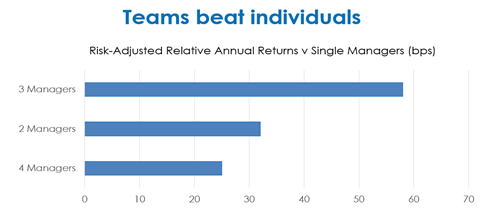

However, as the data in the chart below shows, mutual funds managed by multiple managers perform better on average than those managed by a single person. Given the scale of the information processing challenge implicit in portfolio management, it makes sense that well-constructed teams outperform individuals.

Source: Credit Suisse

This was borne out in work done by academic Klaas Baks who found 70% of mutual fund returns were due to the firm and only 30% to individual fund managers. Yet, as with stockbroking, specific individuals can be rewarded with millions of dollars.

With this in mind, and with my goal of being able to add rigour to the idea that we had a great team, I asked Ben if he would look at Platinum, as if we were a sporting team and in 2017, we became Gain Line’s first corporate client.

This exercise prompted me to look into how knowledge businesses generally, and fund managers specifically, might be organised, and how this could be applied by others.

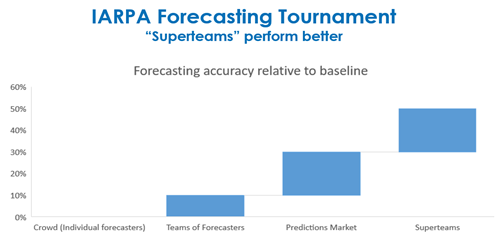

The academic, Philip E Tetlock conducted an interesting study between 1984 and 2003 and concluded that expert forecasts in aggregate were about as useful as dart throwing monkeys. He followed this up in 2015 with a book, Superforecasting – The Art and Science of Prediction, co-authored with Dan Gardner, highlighting elite groups that consistently outperformed.

These two observations may confirm simultaneously the passive view that the average manager does not add value, whilst emphatically reinforcing that the best active managers perform much better over the long run.

In Superforecasting, it emerged that teams were better than individuals were, and he next explored these ’superteams‘. The chart below shows that they performed much better.

Source: Philip E Tetlock & Dan Gardner, Superforecasting: The Art and Science of Prediction

While ‘active open-mindedness’ was key for individuals, team communication patterns, and a sharing culture were additionally important. Diversity of experiences also helps – not simply for the different opinions. A feedback loop forms from everyone refining their forecasts by understanding what others contribute that they themselves lack. This is an iterative process.

Tetlock observed the formation of mini-cultures whereby members challenged each other’s views respectfully, admitted ignorance and requested help. Verbally they used ‘our’ more than ‘my’.

At Platinum, we have described our process as an ‘engaged debate’. We believe there is a huge amount of value in understanding and exploring internal disagreements. Others have talked of ‘constructive confrontation’ or ‘assertive open-mindedness’.

In order to achieve better outcomes in knowledge businesses, team members must co-operate and collaborate. The team must be built correctly for this to happen.

So how can we build a team that is co-operative and collaborative?

Free-flow of information is vital, and it must be safe to challenge and to disagree. This needs certain types of people who can take part in this engaged debate – in Platinum’s case we look for analysts who are curious and love business.

Shared goals and aligned remuneration systems is necessary – it must be all about the client outcome. People need to focus less on themselves and more on the system. We need the right people and the right rewards - the hard part is putting that team together.

Hiring decisions must seek to improve team creation and drive better outcomes.

The key human resources question becomes develop or churn? The common mistake is to hire like-for-like – for example, when a senior person leaves or is removed they are often replaced by an external candidate – when the data suggests we need to promote internally and hire a junior to develop. Senior hires, often brought in to great fanfare, may have the power to change successful systems to suit their own ways. They do this to make it easier for themselves. But they can quickly destroy teams that have taken years to build.

Sporting transfer markets overvalue players from great teams. Investment management is no different. People overpay to hire analysts from good firms. CVs emphasise the most highly regarded firms people have worked for. Rescuing good analysts from poor firms and hiring people with the right attributes early in their careers is a key way to build a sustainable team.

Hire the character not the CV.

If you are in, or are running, a team with poor cohesion metrics, managing stakeholder expectations is paramount. Sadly, not everyone has the patience to wait for the team to develop and meld. But, by not waiting, the outcomes can be much worse. Observe the chaos at the top of numerous large Australian corporates and worry about how long it will take to fix them. Quick fixes do not work.

We need to consider, preferably quantitatively and with benchmarking for the field of candidates:

-

How much collective experience does the team have working together in this company?

-

How much direct external experience did they bring (remembering it is a negative attribute)? Key hires can disappoint.

-

How is the team structured – what internal relationships do people have? Small groups are better than large ones – for example, ‘teams of teams’.

-

When people leave, scrutinise their true contribution. Be careful not to over-value people leaving good firms. Strong teams are resilient to the loss of individuals.

Go beyond perceived competence. Look past simple years of experience, or apparently valuable brand names on CVs. Focus on connections, relationships and dynamics within the system. Focus on how teams are built.

To conclude:

- Cohesion can, and should be, measured.

- Cohesion helps under pressure, increases loyalty and improves skill development.

- Teams can be built to improve cohesion but this cannot be rushed.

- Building a mutual understanding and trust takes time.

- The benefits of pure, shared experience are under-appreciated.

- Define the system and hire people of character to drive the culture.

There is plenty of material to read to expand your thinking and as a passionate advocate of cohesion, I would be happy to build a dialogue with you, so please reach out if you are interested in discussing this topic any further.

Further reading:

- Boris Groysberg, Chasing Stars: The Myth of Talent and the Portability of Performance

- Philip E Tetlock & Dan Gardner, Superforecasting: The Art and Science of Prediction

- TED Talk: Margaret Heffernan, Forget the Pecking Order at Work

- Ben Darwin, Cohesion Analytics: Winning Starts at the Board (accessible at platinum.com.au)

https://www.platinum.com.au/The-Journal/Cohesion-with-Ben-Darwin-(Video)

- Klaas Baks, On the Performance of Mutual Fund Managers

- Saurin Patel and Sergei Sarkissian, To Group or Not to Group? Evidence from Mutual Fund Databases

- Roger Nierenberg, Maestro

- Michael Maubusson, Form over Function (published as Credit Suisse research)

- Douglas Isles, All Blacks: The Outcome of a System (accessible at platinum.com.au)

DISCLAIMER: This article has been prepared by Platinum Investment Management Limited ABN 25 063 565 006, AFSL 221935, trading as Platinum Asset Management (“Platinum”). This information is general in nature and does not take into account your specific needs or circumstances. You should consider your own financial position, objectives and requirements and seek professional financial advice before making any financial decisions. The commentary reflects Platinum’s views and beliefs at the time of preparation, which are subject to change without notice. No representations or warranties are made by Platinum as to their accuracy or reliability. To the extent permitted by law, no liability is accepted by Platinum for any loss or damage as a result of any reliance on this information.

From the journal

Lessons with an investment professional - nine more tips

Douglas Isles' tips explore the hidden dangers of a headline and the power of quality.

Investment lessons with a pro - the front nine

Doug Isles draws on 18 years' experience to talk cliches, hype and the perils of past performance

Scottie Scheffler and the ‘happy amateur’ investor

What can investors learn from the distinction between amateur and professional sport?

It’s a living thing – investing in biologics

Adrian Cotiga explains the rationale behind Platinum's investment in biologics company Lonza.

Subscribe to Platinum

Receive our expert investment insights and market updates.

Journal Articles

Read market leading insights.

Market Updates

Get market updates from our analysts

Quarterly Reports

Receive quarterly investment reports