The SaaS Survivors: Finding Quality Beyond the Hype

Jimmy Su

Portfolio Manager, Platinum International Technology Fund

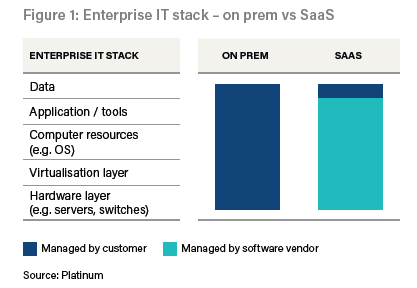

One of the transformative changes in the software industry over the past two decades has been the development of software as a service (SaaS). SaaS is a software delivery model where the vendor develops a web-based application hosted and operated for customers. This is distinctly different from on premise deployment (on prem), where the application is managed by the customer and run on a local server or users’ device.

SaaS deployment has many benefits for end customers. The total lifecycle cost of owning the software is significantly cheaper. Upfront costs are lower as customers don’t need to buy infrastructure hardware (e.g. expensive servers) or pay a high upfront license cost for the software. To see the scale of that change, consider that Adobe Creative Cloud is now available for US$59 a month, whereas customers paid US$2,599 for Creative Suite in 2014. Ongoing maintenance costs are also lower as the majority of system admin tasks are outsourced. SaaS also gives customers better security, network resilience and the flexibility to scale capacity up or down.

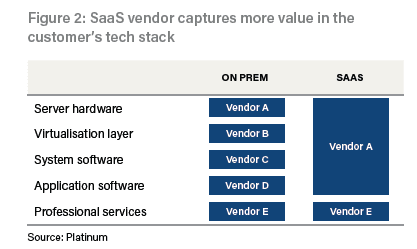

SaaS also offers software vendors many benefits. Over a customer’s lifetime, SaaS vendors typically generate more revenue per customer vs on prem as they capture more value in the IT tech stack (see Figure 2 below) from hardware vendors (e.g. Dell) and system software providers (e.g. Windows server OS). Most software companies cite a revenue uplift of 2-3x. Operating costs are also lower as running multiple customers on a single software instance on multiple servers reduces operational complexity and the cost of managing the software. Finally, lower upfront costs greatly expand the addressable market.

The transition from on prem to SaaS continues to generate investment opportunities. Companies with large existing on prem customers that are in the process of transitioning into SaaS should have a long revenue growth run-way due to the 2-3x revenue uplift mentioned above. This includes customer contact centre software, industrial software and back office enterprise applications which involve complex migrations (e.g. ERP, database software, supply chain).

As investors we need to be thoughtful about this opportunity as transitioning customers to SaaS doesn’t automatically improve profitability for vendors. Absent strong competitive advantages – or ‘moats’ – the aforementioned 2-3x revenue uplift can be competed away. As outlined in Information Rules,1 in software markets where there is low marginal cost and strong lock-in, competition erodes excessive profits out of the market (on a life-cycle basis) as vendors lose money upfront to lock customers in.

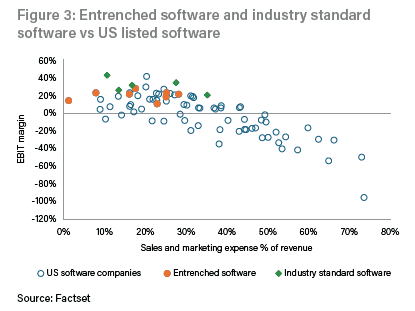

This theory is evident in the data. On 2023 data, only about 50% of listed US software companies make money on a GAAP EBIT basis and only ~30% make margins in excess of 15%. The key determinant of profitability is the upfront sales and marketing spend to acquire customers.

Which SaaS businesses could be winners – and why

As we wrote previously, we like investing in software vendors with strong moats that keep sales and marketing costs in check and allow them to extract excess profits from customers. One set are what we call entrenched software businesses. These are not only mission critical for customers. They also have the strongest ‘lock in’ among peers and customers loathe switching due to the cost, complexity and headache involved.

Our other preference is for industry standard software businesses. Not only are their applications mission critical and entrenched, they also enjoy strong network effects due to broad industry adoption and need for interoperability (e.g. sharing files on Microsoft Office). As Figure 3 shows, profitability among these two cohorts – where sales and marketing costs are relatively low – are either best-in-class, or could be in the future.

Today over 10% of the Platinum International Technology Fund is invested in software companies where on prem penetration remains high, where there is a long run-way for revenue growth as customers transition to SaaS and where the business fit into the “entrenched software” or “Industry standard software” business models. These include SAP, the leader in mission critical ERP software, NICE, a share winner in contact centre software and Computer Modelling Group, a provider of reservoir simulation software for unconventional oil extraction.

Learn more about Platinum’s International Technology Fund

Explore how the Fund invests in businesses shaping the future of software, AI, semiconductors and global technology innovation.

Share this

1. One of our favourite books on software and tech by Carl Shapiro and Hal Varian

Disclaimer:

The above information is commentary only (i.e. our general thoughts). It is not intended to be, nor should it be construed as, investment advice. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Before making any investment decision you need to consider (with your financial adviser) your particular investment needs, objectives and circumstances.

Related Journals

View all related reads

AI’s Spending Boom: Opportunity or Overreach?

The AI investment boom is accelerating, but questions remain around long-term returns, sustainability and who ultimately captures the value. Jimmy Su explores why the current AI capex cycle could still have further to run — despite growing market scepticism.

Apple’s AI Moment of Truth

Apple dominated the smartphone era, but artificial intelligence could represent a far more disruptive platform shift. Jimmy Su explores whether Apple’s strengths, including its ecosystem, brand and privacy-first approach, are enough to compete in the AI age.